Main Menu

Main Menu |

|

Most Favorited Images |

|

Recently Uploaded Images |

|

Most Liked Images |

|

Top Reviewers |

| cockalatte |

646 |

| MoneyManMatt |

490 |

| Still Looking |

399 |

| samcruz |

399 |

| Jon Bon |

396 |

| Harley Diablo |

377 |

| honest_abe |

362 |

| DFW_Ladies_Man |

313 |

| Chung Tran |

288 |

| lupegarland |

287 |

| nicemusic |

285 |

| Starscream66 |

281 |

| You&Me |

281 |

| George Spelvin |

265 |

| sharkman29 |

255 |

|

|

Top Posters |

| DallasRain | 70796 | | biomed1 | 63313 | | Yssup Rider | 61032 | | gman44 | 53296 | | LexusLover | 51038 | | offshoredrilling | 48678 | | WTF | 48267 | | pyramider | 46370 | | bambino | 42769 | | CryptKicker | 37222 | | The_Waco_Kid | 37116 | | Mokoa | 36496 | | Chung Tran | 36100 | | Still Looking | 35944 | | Mojojo | 33117 |

|

|

09-19-2014, 10:25 AM

09-19-2014, 10:25 AM

|

#1

|

|

Account Disabled

Join Date: Apr 7, 2010

Location: Texas

Posts: 5,249

|

Affordable Health Care Act and The End of the World

Affordable Health Care Act and The End of the World

What happened Whirlytard? Admiral? The rest of you half-wits who predicted the end of the world was coming with the passage and implementation of the act?

Let me guess: it will happen in a few more months? Or, surely if another democrat is elected as POTUS in 2016?

And....and....and.....those promises about repealing the act.....and all the light and sound and effort and energy that the house GOP loonies put into repealing the act.....what's the status?

Chirp.....Chirp......Chirp

|

|

Quote

| 1 user liked this post |

|

09-19-2014, 10:56 AM

|

#2

|

|

Account Disabled

Join Date: Jan 20, 2010

Location: Houston

Posts: 14,460

|

Is this another Timmietard Troll Thread? Where you start it and go away for a few days never to respond?

If Obamacare is so great, why did Obama permanently postpone the Business Mandate?

Why did Obama move the sign up period for next year until AFTER the Nov 4 election?

|

|

|

Quote

| 2 users liked this post |

|

09-19-2014, 11:18 AM

|

#3

|

|

Valued Poster

Join Date: Jan 3, 2010

Location: South of Chicago

Posts: 31,214

|

Keep holding your breath, Little Timmy-tard: you apparently seem to like living in a "blue-in-the-face", oxygen deprived environment where your brain cells die.

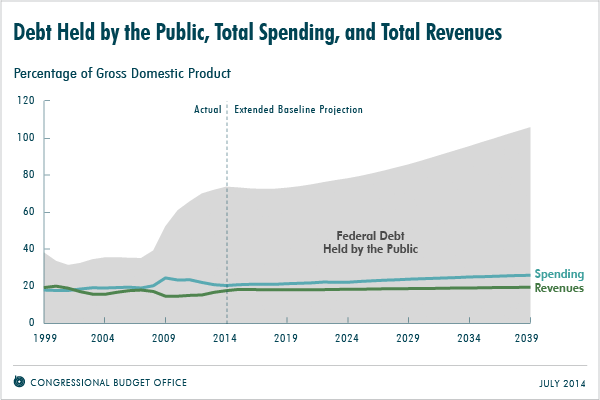

Federal spending would increase to 26 percent of GDP by 2039 under the assumptions of the extended baseline, CBO projects, compared with 21 percent in 2013 and an average of 20½ percent over the past 40 years. That increase reflects the following projected paths for various types of federal spending if current laws remained generally unchanged (see the figure below):

- Federal spending for Social Security and the governments major health care programsMedicare, Medicaid, the Childrens Health Insurance Program, and subsidies for health insurance purchased through the exchanges created under Odumbocare would rise sharply, to a total of 14 percent of GDP by 2039, twice the 7 percent average seen over the past 40 years. That boost in spending is expected to occur because of the aging of the population, growth in per capita spending on health care, and an expansion of federal health care programs.

- The governments net interest payments would grow to 4½ percent of GDP by 2039, compared with an average of 2 percent over the past four decades. Net interest payments would be larger than that average mainly because federal debt would be much larger.

The gap between federal spending and revenues would widen after 2015 under the assumptions of the extended baseline, CBO projects. By 2039, the deficit would equal 6½ percent of GDP, larger than in any year between 1947 and 2008, and federal debt held by the public would reach 106 percent of GDP, more than in any year except 1946even without factoring in the economic effects of growing debt.

http://www.cbo.gov/publication/45471

|

|

|

Quote

| 1 user liked this post |

|

09-19-2014, 11:24 AM

|

#4

|

|

Account Disabled

Join Date: Jun 19, 2011

Location: Dixie Land

Posts: 22,098

|

Timmy you are so full of shit...

http://dailycaller.com/2014/09/15/st...xchange-plans/

When millions of people were losing their health insurance plans in late 2013, Obamacare supporters claimed those plans were of poor quality, calling them substandard and even crappy, Dr. David Hogberg, the studys author, said in a statement. But they never provided any evidence to support those claims. Quite the contrary, this study shows that in important ways, the plans on the individual market in 2013 were of better quality than those on the Obamacare exchanges.

.

|

|

|

Quote

| 1 user liked this post |

|

09-19-2014, 12:18 PM

|

#5

|

|

Lifetime Premium Access

Join Date: Jan 1, 2010

Location: houston

Posts: 48,267

|

We need to cut Defense Spending....no other way around it.

Under yet another scenario, with twice as much deficit reduction—a total decrease of $4 trillion in deficits excluding interest payments through 2024—CBO projects that federal debt held by the public would fall to 42 percent of GDP in 2039. That percentage would be slightly above the ratio of debt to GDP in 2008 and the average ratio over the past 40 years (both 39 percent). As in the preceding scenario, output would be higher and interest rates would be lower in the long term than under the extended baseline.

.

|

|

|

Quote

| 1 user liked this post |

|

09-19-2014, 12:32 PM

|

#6

|

|

Account Disabled

Join Date: Jan 3, 2010

Location: Here.

Posts: 13,781

|

Yep.

And why did Obama and the Democrats have to lie to pass a piece of legislation that was so damn great?

Oh yeah, and Obamacare enrollments are declining...I guess enrollees are finding out what was in it and what it really costs.

http://www.latimes.com/nation/nation...918-story.html

Quote:

Originally Posted by gnadfly

Is this another Timmietard Troll Thread? Where you start it and go away for a few days never to respond?

If Obamacare is so great, why did Obama permanently postpone the Business Mandate?

Why did Obama move the sign up period for next year until AFTER the Nov 4 election?

|

|

|

|

Quote

| 1 user liked this post |

|

09-19-2014, 02:24 PM

|

#7

|

|

Account Disabled

Join Date: Jun 19, 2011

Location: Dixie Land

Posts: 22,098

|

Quote:

Originally Posted by WTF

Under yet another scenario, with twice as much deficit reductiona total decrease of $4 trillion in deficits excluding interest payments through 2024CBO projects that federal debt held by the public would fall to 42 percent of GDP in 2039. That percentage would be slightly above the ratio of debt to GDP in 2008 and the average ratio over the past 40 years (both 39 percent). As in the preceding scenario, output would be higher and interest rates would be lower in the long term than under the extended baseline.

.

|

here you go... http://www.cbo.gov/publication/45471

.

|

|

|

Quote

| 1 user liked this post |

|

09-19-2014, 04:53 PM

|

#8

|

|

Valued Poster

Join Date: Jan 16, 2010

Location: Texas

Posts: 51,038

|

I think WTF et al .. need SLIDES:

http://www.cbo.gov/publication/45527

It's more like TV cartoons.

|

|

|

Quote

| 2 users liked this post |

|

09-19-2014, 08:43 PM

|

#10

|

|

Lifetime Premium Access

Join Date: Jan 1, 2010

Location: houston

Posts: 48,267

|

Quote:

Originally Posted by LexusLover

|

You need reading glasses.

Quote:

Originally Posted by WTF

Under yet another scenario, with twice as much deficit reductiona total decrease of $4 trillion in deficits excluding interest payments through 2024CBO projects that federal debt held by the public would fall to 42 percent of GDP in 2039. That percentage would be slightly above the ratio of debt to GDP in 2008 and the average ratio over the past 40 years (both 39 percent). As in the preceding scenario, output would be higher and interest rates would be lower in the long term than under the extended baseline.

.

|

|

|

|

Quote

| 1 user liked this post |

|

09-19-2014, 11:55 PM

|

#11

|

|

Account Disabled

Join Date: Jun 19, 2011

Location: Dixie Land

Posts: 22,098

|

Quote:

Originally Posted by Yssup Rider

|

Obama Bin Lyin ain't the only one... You too, Hissy Fit

http://www.theblaze.com/stories/2014...red-americans/

How Obamacare Could Increase the Number of Uninsured Americans

Jun. 11, 2014 7:01pm Fred Lucas

A forthcoming academic report is warning that in 10 years, 40 million Americans will be without health insurance a 10 percent increase and Obamacare will be to blame.

It says that after 2017, health insurance premiums will escalate so high that an increasing number of employers will opt to pay the less expensive fine, and the individuals, finding few affordable options on the exchanges, will choose to do the same by 2024.

The report is by Bianca Frogner, assistant professor for health services management and leadership at George Washington University, and Stephen Parente, associate dean of the Carlson School of Management and director of the Medical Industry Leadership Institute at the University of Minnesota.

There will be a significant number of uninsured Americans unwilling or unable to pay for the inflated insurance available on the exchanges and forced to pay penalties, which for 2016 and thereafter will be the greater of $695 or 2.5 percent of income, Parente wrote in a Wall Street Journal op-ed previewing the report. More will choose this option every year. By 2024, Ms. Frogner and I estimate that there will be more than 40 million uninsured, roughly 10 percent more than today.

The projections from experts in their field could sting more than those from Republican politicians. The assessment comes in the midst of a tough election year for Democrats, who insist the debate over the Affordable Care Act is over because 8 million signed up for the healthcare.gov exchanges.

Based on 2014 health insurance exchange enrollment data, the authors estimate the impact of Obamacare from 2015-2024. They determined the average premium for a silver plan will increase by $4,198 for a family by 2019 and increase by $1,375 for an individual.

That outpaces the average rate of increase from 2008 to 2013, before the health law was implemented. Obama administration officials, while conceding premiums are increasing, have argued the Affordable Care Act will keep the rate of increase down.

Meanwhile, the Congressional Budget Office estimates that Obamacare will lead to 7 million people being dropped from employer-provided insurance by 2020. This will drive more people to the Healthcare.gov exchanges, which will drive up the cost of those plans.

We estimate that Medicaid enrollment will increase by 2 percent to 3 percent annually through 2024. Yet this will not capture everyone, Parente wrote. Many will not be eligible for the program, because either they earn more than 133% of the federal poverty level (currently $11,670 for an individual, $23,850 for a family of four) or their state did not expand Medicaid.

The professors predict the steepest price increases will not occur until 2017.

Thats when the hardship exemptions from all existing plans will expire. Also that year, health insurers will not be able to bill the government 80 percent of a patients cost when a makes more than $45,000 in annual claims.

The multibillion-dollar risk corridors for insurance companies will also sunset in 2017ending the taxpayer bailouts that kick in when insurance companies providing ACA plans lose money, Parente wrote. Insurance companies will have neither option by 2017, leaving consumers to pick up the tab through premium payments. Federal subsidies will be unable to keep up with such dramatic rate spikes.

He went on to write: Confronted with this cost crisis, consumers will react the only way they know how: by looking for cheaper options such as the remaining high-deductible health plans offered by private companies and the exchanges as well as plans with very limited physician and hospital networks geared to achieve maximum efficiency for the average patient. These plans are likely to provide no or limited access to specialized facilities and physicians. Rising premiums will create a cyclical exodus from insurance plans, with each wave of departures fueling premium spikes that cause even more departures.

|

|

|

Quote

| 1 user liked this post |

|

09-20-2014, 12:06 AM

|

#12

|

|

Premium Access

Join Date: Jan 8, 2010

Location: Steeler Nation

Posts: 18,670

|

Hey Timmytard, let's get down and dirty here. Tell us about those "RISK CORRIDOR" PAYMENTS to the insurance companies. How many federal dollars are flying out the door under this carte blanche Odumbocare provision?

ObamaCare and American Decline

America needs a change of direction domestically to cope with a dangerous and disorderly world.

By Holman W. Jenkins, Jr.

Sept. 16, 2014 7:53 p.m. ET

The reports of Darrell Issa's House Oversight and Government Reform Committee are a clinic on how government is really run. The latest on ObamaCare is no exception.

We see Chet Burrell, head of Maryland insurer CareFirst, emailing in alarm last April to White House aide Valerie Jarrett. The administration had just publicly stated its "risk corridor" plan would be revenue neutral—i.e., no extra taxpayer dollars would be available to cover insurer losses.

We see Mr. Burrell warning that sticking with this plan would mean politically "an unwelcome surprise," namely premium hikes of 20% or more later this year as ObamaCare policies come up for renewal.

We see Ms. Jarrett emailing back in concern. We see her later assuring Mr. Burrell that insurers would get 80% of what they sought. After another program tweak in May, the figure would be closer to 100%.

Sure enough, this week came the fallout. Bob Laszewski, a policy wonk and former insurance executive whose bloggings are closely followed in the ObamaCare debate, writes that the administration has succeeded in temporarily suppressing incipient ObamaCare price hikes, contributing to an illusion of sustainability. He suggests that some insurers might even slash rates to "grab market share because they have nothing to lose with the now unlimited ObamaCare reinsurance program covering their losses."

The non-surprise revealed here is that ObamaCare turns out to be just another subsidy program, throwing money at health care. In economics, you can't subsidize everybody but we're trying: 50 million Americans get help from Medicare, 65 million from Medicaid, nine million from the Department of Veterans Affairs, seven million (and counting) from ObamaCare, and a whopping 149 million from the giant tax handout for employer-provided health insurance.

Much of this money (which will total about $1.3 trillion in 2014) is shoveled out regardless of need, driving up prices and spurring production of services of dubious value. The spending is less effective at improving the nation's health. An "Affordable Care Act" worth its title would have gotten us off this kamikaze mission. It didn't.

Then there's Halbig v. Burwell . This is the latest legal threat to ObamaCare's improvisational unfolding. At issue is whether the words in the law mean anything—i.e., whether Congress in fact authorized the subsidies the administration has been doling out to users of the federally run (as opposed to state-run) health-care exchanges.

A cosmic test of any administration is whether it can escape town before its misplaced priorities catch up with it. An obvious Halbig solution would be for Congress simply to clarify what the words mean—except the House is now controlled by a party not a single member of which voted for ObamaCare.

The president, meanwhile, is weakened by a deteriorating world situation while he focused on "nation building at home"—by which he meant ObamaCare. He is weakened by U.S. companies accelerating their flight abroad from an unreformed U.S. tax system—because the only reform Mr. Obama was interested in was ObamaCare.

What will the president's legacy be if not ObamaCare? A fracking boom he had nothing to do with? His threadbare claim to have rescued the economy from the 2008 meltdown?

ObamaCare has become his Ukraine. It cost his party control of Congress. It might have cost him re-election if Republicans hadn't nominated somebody who reminded Americans of everything they hate about Wall Street. It barely squeaked past the Supreme Court. It got him sued by the House speaker. It has required ever-more flagrantly lawless exercises of executive power. Even the IRS scandal has its roots in ObamaCare—recall that Lois Lerner was allegedly tasked with suppressing tea party activity in the runup to 2012.

Halbig, which remains to be adjudicated by the appeals system, may be a very big deal for the administration (to modify Joe Biden's phrase). But it's not a big deal for health-care reform, the unstarted work of closing the gap between cost and benefit so the U.S. can avoid bankrupting itself. Suddenly luminous is the true historical significance of ObamaCare: A left-liberal president, in the backwash of a global economic crisis that he could plausibly blame on Wall Street, could not get a "public option" through an all-Democratic Congress.

The high tide for single payer has come and gone in America. The action now moves permanently to the challenge of paying for existing welfare programs, not creating new ones.

This connects to another Obama legacy, a more dangerous and disorderly world. A world in which America needs to tighten up and toughen up. A world in which rising powers (e.g., China) no longer can be expected to finance endless American deficits so Americans can spend somebody else's money on health care. Election 2016 can't come fast enough for an America that needs a radical change of direction to cope with a changing world.

.

|

|

|

Quote

| 2 users liked this post |

|

09-20-2014, 12:25 AM

|

#13

|

|

Account Disabled

Join Date: Jun 19, 2011

Location: Dixie Land

Posts: 22,098

|

Quote:

Originally Posted by lustylad

Hey Timmytard, let's get down and dirty here. Tell us about those "RISK CORRIDOR" PAYMENTS to the insurance companies. How many federal dollars are flying out the door under this carte blanche Odumbocare provision?

ObamaCare and American Decline

America needs a change of direction domestically to cope with a dangerous and disorderly world.

By Holman W. Jenkins, Jr.

Sept. 16, 2014 7:53 p.m. ET

The reports of Darrell Issa's House Oversight and Government Reform Committee are a clinic on how government is really run. The latest on ObamaCare is no exception.

We see Chet Burrell, head of Maryland insurer CareFirst, emailing in alarm last April to White House aide Valerie Jarrett. The administration had just publicly stated its "risk corridor" plan would be revenue neutrali.e., no extra taxpayer dollars would be available to cover insurer losses.

We see Mr. Burrell warning that sticking with this plan would mean politically "an unwelcome surprise," namely premium hikes of 20% or more later this year as ObamaCare policies come up for renewal.

We see Ms. Jarrett emailing back in concern. We see her later assuring Mr. Burrell that insurers would get 80% of what they sought. After another program tweak in May, the figure would be closer to 100%.

Sure enough, this week came the fallout. Bob Laszewski, a policy wonk and former insurance executive whose bloggings are closely followed in the ObamaCare debate, writes that the administration has succeeded in temporarily suppressing incipient ObamaCare price hikes, contributing to an illusion of sustainability. He suggests that some insurers might even slash rates to "grab market share because they have nothing to lose with the now unlimited ObamaCare reinsurance program covering their losses."

The non-surprise revealed here is that ObamaCare turns out to be just another subsidy program, throwing money at health care. In economics, you can't subsidize everybody but we're trying: 50 million Americans get help from Medicare, 65 million from Medicaid, nine million from the Department of Veterans Affairs, seven million (and counting) from ObamaCare, and a whopping 149 million from the giant tax handout for employer-provided health insurance.

Much of this money (which will total about $1.3 trillion in 2014) is shoveled out regardless of need, driving up prices and spurring production of services of dubious value. The spending is less effective at improving the nation's health. An "Affordable Care Act" worth its title would have gotten us off this kamikaze mission. It didn't.

Then there's Halbig v. Burwell . This is the latest legal threat to ObamaCare's improvisational unfolding. At issue is whether the words in the law mean anythingi.e., whether Congress in fact authorized the subsidies the administration has been doling out to users of the federally run (as opposed to state-run) health-care exchanges.

A cosmic test of any administration is whether it can escape town before its misplaced priorities catch up with it. An obvious Halbig solution would be for Congress simply to clarify what the words meanexcept the House is now controlled by a party not a single member of which voted for ObamaCare.

The president, meanwhile, is weakened by a deteriorating world situation while he focused on "nation building at home"by which he meant ObamaCare. He is weakened by U.S. companies accelerating their flight abroad from an unreformed U.S. tax systembecause the only reform Mr. Obama was interested in was ObamaCare.

What will the president's legacy be if not ObamaCare? A fracking boom he had nothing to do with? His threadbare claim to have rescued the economy from the 2008 meltdown?

ObamaCare has become his Ukraine. It cost his party control of Congress. It might have cost him re-election if Republicans hadn't nominated somebody who reminded Americans of everything they hate about Wall Street. It barely squeaked past the Supreme Court. It got him sued by the House speaker. It has required ever-more flagrantly lawless exercises of executive power. Even the IRS scandal has its roots in ObamaCarerecall that Lois Lerner was allegedly tasked with suppressing tea party activity in the runup to 2012.

Halbig, which remains to be adjudicated by the appeals system, may be a very big deal for the administration (to modify Joe Biden's phrase). But it's not a big deal for health-care reform, the unstarted work of closing the gap between cost and benefit so the U.S. can avoid bankrupting itself. Suddenly luminous is the true historical significance of ObamaCare: A left-liberal president, in the backwash of a global economic crisis that he could plausibly blame on Wall Street, could not get a "public option" through an all-Democratic Congress.

The high tide for single payer has come and gone in America. The action now moves permanently to the challenge of paying for existing welfare programs, not creating new ones.

This connects to another Obama legacy, a more dangerous and disorderly world. A world in which America needs to tighten up and toughen up. A world in which rising powers (e.g., China) no longer can be expected to finance endless American deficits so Americans can spend somebody else's money on health care. Election 2016 can't come fast enough for an America that needs a radical change of direction to cope with a changing world.

.

|

SLAM FUCKING DUNK!

|

|

|

Quote

| 1 user liked this post |

|

09-20-2014, 12:26 AM

|

#14

|

|

Valued Poster

Join Date: Jun 25, 2012

Location: Ahead of you.

Posts: 856

|

Another article on Daily Caller had this to say:

"Obamacare administrator Marilyn Tavenner admitted that several months after the open enrollment period ended, the number of paying customers has dropped precipitously.

By August 15, over 700,000 of the administration’s initial “sign-ups” had dropped their Obamacare coverage, Tavenner said in testimony to the House Oversight Committee. The administration has been advertising 8 million sign-ups since the first enrollment period ended in April."

http://dailycaller.com/2014/09/18/70...heir-coverage/

|

|

|

Quote

| 1 user liked this post |

|

09-20-2014, 12:52 AM

|

#15

|

|

Valued Poster

Join Date: Jun 12, 2011

Location: Olathe

Posts: 16,815

|

I'm not sure what he's going on about. Obamacare has failed and failed miserably. Later this month about another 400,000 people are going to lose their Obamacare because they are not citizens and more are going to lose their subsidy because they make too much. Seems that they couldn't check on this stuff back at the beginning of the year.

Also, the official enrollment stands at 7.3 million which is a whole lot less than the 40 million that needed this healthcare (not really healthcare but just insurance for what that's worth) so bad that they had to screw things up for the rest of us.

|

|

|

Quote

| 1 user liked this post |

|

|

AMPReviews.net |

|

Find Ladies |

|

Hot Women |

|